Table of Content

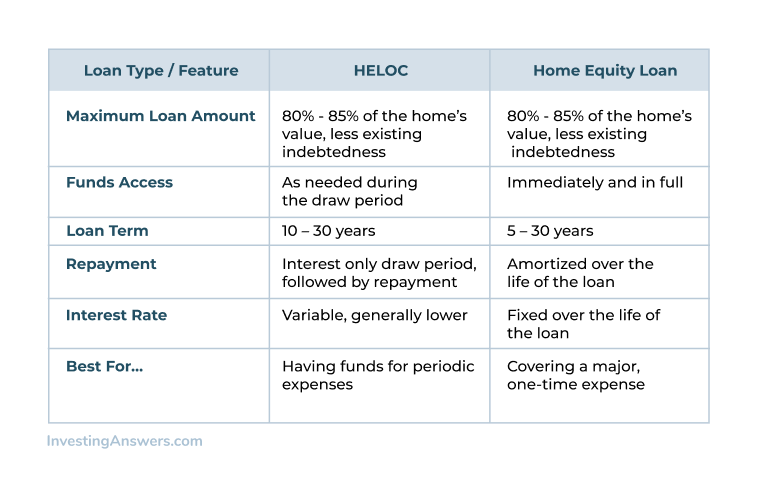

A home equity loan is a type of loan in which the borrowers use the equity of their home as collateral. The loan amount is determined by the value of the property, and the value of the property is determined by an appraiser from the lending institution. A piggyback mortgage can include any additional mortgage loan beyond a borrower’s first mortgage loan that is secured with the same collateral. With a home equity loan, the borrower receives the loan proceeds all at once, while a HELOC allows a borrower to tap into the line as needed. Because the amount borrowed can change , the borrower’s minimum payments can also change, depending on the credit line’s usage. It allows the borrower to take out money against the credit line up to a preset limit, make payments, and then take out money again.

A home equity loan offers you predictable monthly payments because your interest rate is fixed and never changes. You are on a set repayment schedule and will make the same monthly payment for your whole loan term. If you’re looking for a relatively short-term loan, a 0% APR credit card may be a good option. These credit cards charge zero interest for an introductory period, but the interest rate jumps back to a normal rate after that time. In addition, credit limits will likely be lower than you’d be able to borrow with a home equity loan, and interest rates after the introductory period can be steep. But with a home equity loan, the sum you borrow will be subject to a fixed interest rate.

Balance transfer credit card

If you plan to use a home equity loan to pay off other debts or buy a car, it’s advisable to consider all your options before opting for a loan that could put your primary residence at risk. Nonetheless, it’s always a good idea to speak to a financial advisor to make sure you’ll be able to manage the different types of loans. With higher interest rates, home equity loans come with higher payments.

This is particularly important if you borrow with a HELOC as your monthly payments will change in concert with interest rates. If you’re planning on tapping into your home’s equity, it’s key to have a strategy for how you’ll use and pay back the money you borrow. So, you want to make sure you have room in your budget in case you face job or income loss. It's possible to get more than one home equity loan on your house, but it can be difficult. You'll need to have enough equity in your home to support your primary mortgage and multiple additional loans. Additionally, many lenders won't want to be third in line for repayment if you run into financial troubles.

Bottom line: Are home equity loans a good idea?

Laura has also written for NextAdvisor, MoneyGeek, Personal Finance Insider, and The Financial Diet. Will look at your credit score and payment history to determine the loan interest rate. Her expertise includes mortgages, credit card rewards, and personal finance.

These are common with interest-only loans where your monthly payments do not pay down any of the principal. Be sure you understand your loan terms before you sign on the dotted line. With a cash-out refinance, you owe the amount left on the original mortgage—and you borrow more money against your home’s equity. So, you’re basically going backwards and defeating the purpose of refinancing, which is to get out of debt quicker.

How To Get a Home Equity Loan

With a 15-year mortgage, however, borrowers are able to pay off their loan in half the time — if they’re able and willing to enlarge the amount of their monthly loan payment. If you’re struggling to stay on top of your debts and expenses, a credit counselor can help. Beyond simply offering advice, credit counselors can assist you as you create and execute a debt management plan. During this process, the counselor may help you get discounts from your creditors on interest rates and fees, or lower your monthly payments. The amount you’re able to borrow with a home equity loan is generally set by the amount of equity in your home. You can usually borrow up to 85% of the equity in your home; the more equity you have, the more you’re able to borrow.

You’ll pay interest every month only on the amount you draw with options for interest-only payments. Most of the time HELOCs come with a variable or adjustable interest rate, which is good when rates are low but can be impossible to keep up with if they rise too quickly. A HELOC is a revolving line of credit, much like a credit card, that you can draw on as needed, pay back, and then draw on again, for a term determined by the lender.

Pros and Cons of Borrowing on Home Equity

That means that your monthly payments under that loan will be predictable and won't change over time. You'll also want to be sure that this type of loan makes sense before you borrow. Is it a better fit for your needs than a simple credit card account or anunsecured loan? These other options might come with higher interest rates, but you could still come out ahead by avoiding the closing costs of a home equity loan. A home equity loan, sometimes referred to as a second mortgage, usually allows you to borrow a lump sum against your current home equity for a fixed rate over a fixed period.

How much you can borrow depends on how much home equity you have, your credit score and other factors. A home equity loan calculator can help you estimate how much you might be able to borrow. Every lender operates at its own speed, but since the process to underwrite a home equity loan is similar to a standard mortgage, you can expect it to take about the same amount of time.

Millions of people have used our financial advice through 22 books published by Ramsey Press, as well as two syndicated radio shows and 10 podcasts, which have over 17 million weekly listeners. Most lenders want you to have a loan-to-value ratio that’s 80% or less. If you meet that criteria, they’ll approve you for a loan amount—usually up to 85% of your home equity. They also look at something called your loan-to-value ratio, which compares how much you owe on the house to how much equity you have. Even if you repaid part of the loan, the bank can’t just saw off the master bedroom so you can keep the part of the house you own.

As with a home equity loan, you'd need sufficient equity, but you'd only have one payment to worry about. The lender is approving you for payments you really can't afford—and you know you can't afford them. Remember, the lender gets to repossess your home if you can't make the payments, and you ultimately default. Be sure you can afford your monthly payments by first crunching the numbers. Apply with several lenders and compare their costs, including interest rates.

You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. There are a number of key benefits to home equity loans, including cost, but there are also drawbacks. The interest on a home equity loan is only tax deductible if the loan is used to buy, build, or substantially improve the home that secures the loan. Our star ratings are based on a range of criteria and are determined solely by our editorial team. This information may include links or references to third-party resources or content. We do not endorse the third-party or guarantee the accuracy of this third-party information.

No comments:

Post a Comment